Courtesy of SeafoodNews.com:

This is the first part of a two-part end of year review. Today we will focus on the fantastic year most in the Seafood industry have had, despite the turmoil and disruption of the pandemic.

The second part will look at how the factors that helped us in 2021 may play out in 2022 and what we think may be different.

First, some numbers. When I went to

analyze what happened with the U.S.

seafood supply in 2021, I was blown away by our success.

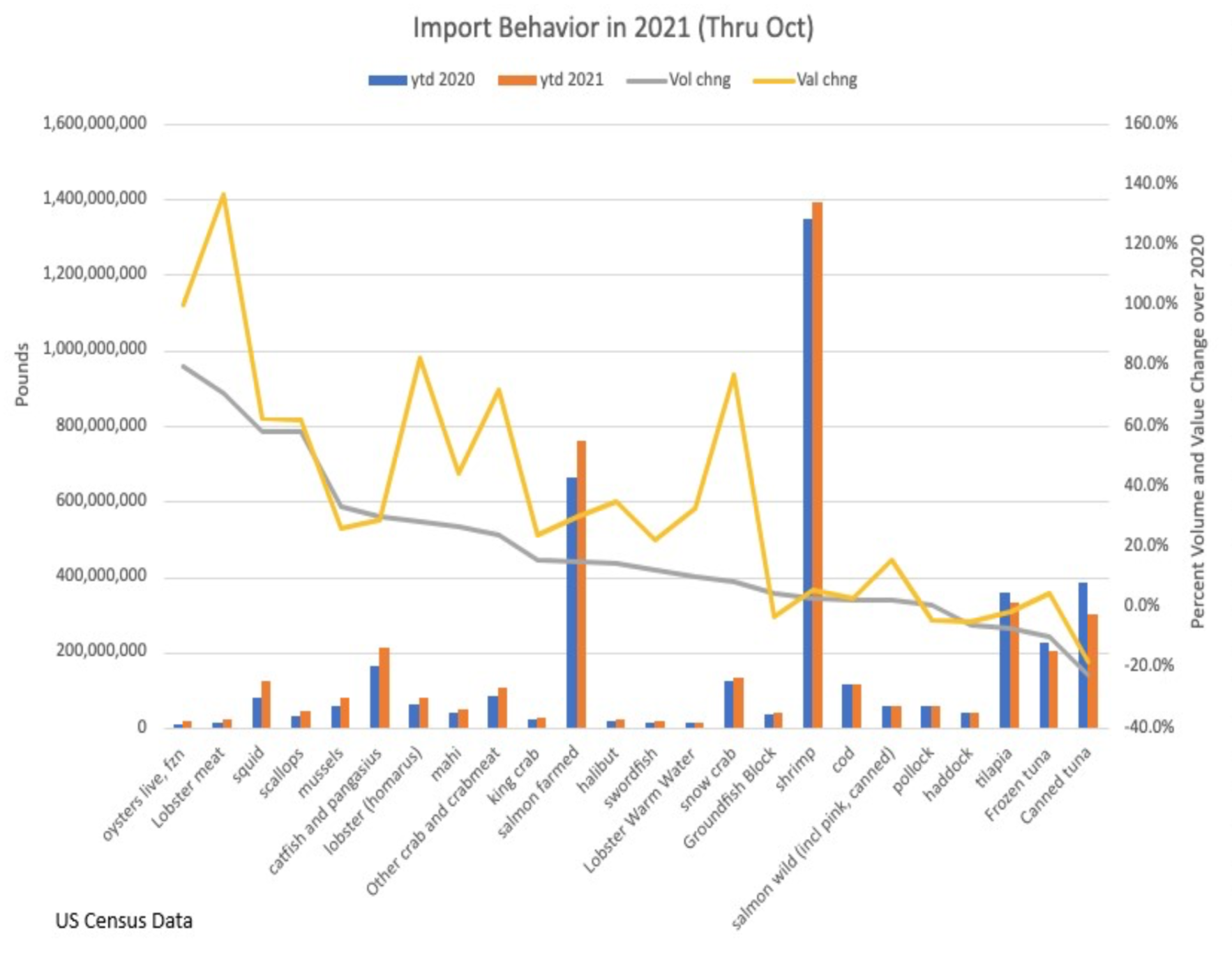

Using the data through October as a proxy for the year, we imported 4.2 billion pounds, 6% over the volume of 2020, and 11% over the volume of 2019. The value of these imports was up a staggering 24% from their values in 2020.

Despite the huge problems of supply chain logistics, the port backups, high freight rates, the lack of truck drivers, lack of containers, full warehouses, and all the other things that make moving seafood from point A to point B a nightmare this year, we handled a record amount of fish.

I have no doubt that when seafood consumption numbers for 2021 are published next summer, we will find another increase in overall consumption.

When I looked at individual species, the increase in imports, and in value, was almost across the board.

For example, out of 24 major commercial products covering virtually all our seafood trade, only three products declined in volume in 2021: tilapia, frozen tuna, and canned tuna.

Everything else was imported at higher volumes.

Products whose import volume jumped more than 20% over 2020 included:

-Oysters

-Lobster Meat

-Squid

-Scallops

-Mussels

-Catfish & Pangasius -Lobster (frozen and live) -Mahi

-Crabmeat

Products where volumes increased 10% to 20% over last year (with data through October 2021) included

-King crab

-Farmed salmon -Halibut

-Swordfish

-Warm water lobster tail

Products where volumes increased between 1% and 9% included

-Snow crab -Groundfish blocks

-Shrimp (with likely record imports for the 7thth year in a row) -Cod

-Wild salmon

-Pollock

-Haddock

Despite the logistics issues and freight disruptions, importers managed to bring in more products across almost their entire inventory.

The values of these imports skyrocketed. Remember value is a combination of increased price and increased volume.

Products where the import values increased by more than 50% included

Lobster meat Oysters Lobster Snow Crab Squid Scallops Crabmeat

Products where the value increased 20% to 50% included

Mussels

Catfish & Pangasius Mahi

King Crab

Farmed Salmon Halibut

Swordfish

Warm Water Lobster

The experience over the past year has been that demand has been so strong as to push up prices even as importers and distributors increased their overall supply.

We know the basic reasons. For the most part seafood held on to its retail sales gains, especially in the frozen category, while at the same time foodservice ordering increased as more restaurants and institutions reopened. At the same time, the industry continued to benefit from the fact that consumers who felt constrained about getting seafood on vacation or in restaurants took the money they had saved and bought seafood to cook at home.

Some of these heavy imports through October may represent early ordering for Lent and an attempt to build up inventory a month or two before normal for the upcoming selling season. But nevertheless, the big picture is that the industry has made a huge effort to increase availability in the face of big increases in demand.

This goes for the domestic industry as well. Although NOAA recently put out a report saying domestic seafood landing revenue was down sharply in 2020, they only had data through July. The most important thing in 2020 was that the industry was able to make adjustments due to Covid and keep operating, even with disruptions. For the full year, anecdotally revenues improved and got closer to normal, but we don’t have data. In 2021, major US fisheries such as Alaska pollock, Alaska salmon, East Coast Lobster, East Coast Scallops, and West Coast Pink shrimp and Dungeness, to name a few, all operated with higher prices and strong demand.

That has not been the case in many other industries which have been more disrupted by supply chain issues. For example, the auto industry is way behind on production. In 2020 they managed to deliver only 14.6 million cars in the US, the lowest number since 2012. And in 2021, they only managed to increase that number by 3%. This is 2 million cars less than the original forecasts for this year of 17 million vehicles. Globally, the auto industry will miss their production targets by about 7 million vehicles for the year, and their problems will continue into 2022.

The reason is the automotive industry has been hampered by a shortage of computer chips that they have no possible way to make up or get around.

I have a theory about why we did so well in comparison to some other industries. I think the reason is that the pandemic supply disruptions that did occur played to our strengths.

We have always operated with an uncertain supply chain. For example, a stock forecast for cod or Alaska pollock is suddenly revised, or a quota is missed, and significant volume evaporates.

Or a Christmas lobster season begins in Nova Scotia, and bad weather keeps the fleet in for 10 days in December.

Or Dungeness openings are delayed due to domoic acid readings or meat fill issues.

Or major shrimp production areas are hit with a disease outbreak.

Or Icelandic cod fishing is suddenly cut back.

All of these things happened in our industry prior to the pandemic, so those who are responsible for supplying programs and meeting customer needs know how to plan for uncertainty and how to work around these problems.

What happened this year was we had to do this on steroids. In most cases it was not production issues but logistical and factory operations that caused problems, expecially with the bottlenecks that developed in China. The good news is that the demand was so strong that the cost increases resulting from these disruptions were understood by our customers, and for the most part they kept purchasing as prices rose.

During a recent Urner Barry seminar on crab and groundfish prices, Mark Kotok of Arctic Fisheries said that as an importer and seafood distributor, every step in his business was significantly harder this year.

Getting product from Asia, unloading at a port, moving the product to a warehouse, moving it out of a warehouse, delivering to a customer was more difficult and expensive due to the impact of the truck driver shortage, and of course the port congestion and container shortage.

At the national level, NFI has been pounding the message in Washington that supply chains are broken, and efforts must be made to fix them.

The skills and flexibility that seafood sellers had developed from their past experiences with disruptions were put into practice this year and the results, both in sales and profitability, speak for themselves.

In the next installment of these year-end columns, I will discuss how this experience may be different next year, other significant changes in the past year, and what our sales environment might be like in 2022.

Photo Credit: Shutterstock/ TanakDusun